| How courts, attorneys, and federal agencies use median household income to calculate damages, determine bankruptcy eligibility, and shape legal outcomes across America. |

What Is Median Household Income? A Legal Definition

Median household income is one of the most consequential economic statistics in American law. It sits at the center of personal injury settlements, wrongful death claims, bankruptcy eligibility determinations, and employment discrimination cases. Yet it is frequently misunderstood, even by litigants and, in some instances, by counsel who do not practice in economically intensive areas of law.

This article explains what median household income means, what it is in the United States and in individual states such as California, and, most critically, how courts and attorneys use it across the full spectrum of U.S. legal proceedings. Whether you are an attorney, paralegal, plaintiff, or defendant, understanding this figure can materially affect the outcome of your case.

Defining Median Household Income vs. Average (Mean) Income

The median household income is the income level at the exact midpoint of all U.S. households ranked from lowest to highest earnings. Exactly half of all households earn more than this figure; exactly half earn less.

This is fundamentally different from average (mean) household income, which adds all household incomes together and divides by the total number of households. Because a small number of extremely wealthy households can pull the mean sharply upward, the mean overstates what a typical American family actually earns. The median is therefore the preferred benchmark in both economics and law whenever the goal is to represent the economic reality of an ordinary person.

| Legal significance: In personal injury and wrongful death litigation, the debate between mean income and median income is not merely academic. It directly determines whether a plaintiff receives more or less compensation for lost earning capacity. German research published through CESifo (Peitz & Schweitzer, 2019) found that mean-based compensation awards can substantially exceed median-based awards, raising fairness and proportionality concerns across jurisdictions. |

What Is the Median Household Income in the U.S.? (2024 Data)

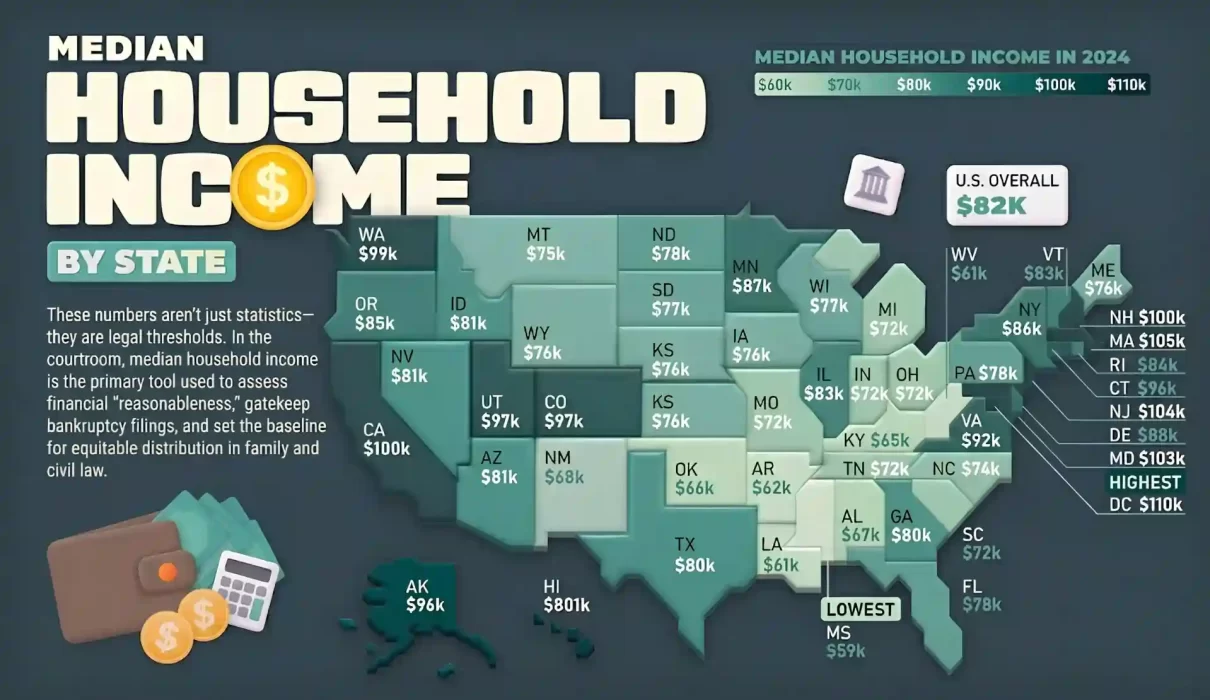

According to the U.S. Census Bureau’s 2025 Current Population Survey Annual Social and Economic Supplement, the national median household income in 2024 was $83,730. This was not statistically different from the 2023 figure of $82,690, indicating relative stability in national household earnings.

Key demographic breakdowns for 2024 include:

- Asian households saw median income rise by 5.1% between 2023 and 2024

- Hispanic households saw a 5.5% increase in median income

- Black households saw a 3.3% decline in median income

- White and non-Hispanic White households saw no statistically significant change

- Full-time, year-round male workers saw median earnings rise by 3.7%, while female workers saw no significant change

- The female-to-male earnings ratio fell to 80.9% in 2024, down from 82.7% in 2023

These disparities are legally significant. They form the evidentiary foundation for employment discrimination lawsuits, equal pay litigation, and systemic bias claims under Title VII of the Civil Rights Act of 1964 and the Equal Pay Act.

Figure 1: Median Household Income by Geography (2024)

| Geography | Median Household Income (2024) | Source |

| United States (National) | $83,730 | U.S. Census Bureau |

| California | $100,100 | USAFacts / Census ACS |

| Maryland | ~$102,000 | Census ACS 2024 |

| Mississippi (lowest) | ~$52,000 | Census ACS 2024 |

| New Jersey (highest) | ~$105,000 | Census ACS 2024 |

What Is the Median Household Income in California?

California consistently ranks among the highest-income states in the nation. According to the 2024 American Community Survey, the median household income in California was $100,100, approximately 22.7% above the national median. FRED data from the Federal Reserve records this figure at $100,600 for the same period.

California’s elevated median income has direct legal implications:

- Higher lost wages claims: Injured plaintiffs in California personal injury cases will typically demonstrate higher economic damages than plaintiffs in lower-income states.

- Higher bankruptcy thresholds: The Chapter 7 bankruptcy means test uses California’s median income to determine eligibility, making it harder for higher-earning Californians to qualify for liquidation-based relief.

- Higher wrongful death damages: California juries calculating the economic loss to surviving family members will use a higher income baseline.

- Employment discrimination benchmarks: California’s Fair Employment and Housing Act (FEHA) claims rely on state-level income data to assess wage gaps and discriminatory pay practices.

Single-person households in California had a median income of $50,786 according to the most recent ACS 5-year estimates, while household income varies dramatically by geography within the state, from high-income tech corridors in Silicon Valley (zip code 94027 averaging $579,268) to significantly lower-income rural counties.

How Courts Calculate Damages Using Median Household Income

Median household income enters litigation through multiple legal doctrines and procedural mechanisms. Below is a comprehensive breakdown of how it functions across the major areas of U.S. law.

Figure 2: Legal Contexts Where Median Household Income Applies

| Legal Context | How Median Household Income Is Used |

| Personal Injury Damages | Baseline for lost wages and future earning capacity calculations |

| Wrongful Death Claims | Calculating economic loss to surviving dependents |

| Bankruptcy Means Test | Chapter 7 eligibility threshold under BAPCPA |

| Employment Discrimination | Benchmark to assess wage disparity and back pay |

| Family Law / Child Support | Determining support obligations and ability to pay |

| Criminal Sentencing (Fines) | Calibrating fines proportional to a defendant’s income level |

| Class Action Settlements | Allocating pro-rata shares among class members |

1. Personal Injury: Lost Wages and Earning Capacity

In personal injury litigation, economic damages are typically the largest and most vigorously contested component of a damages award. They include past lost wages, future lost wages, and diminished earning capacity. All three calculations tie directly to income data.

Courts do not simply accept a plaintiff’s self-reported income. They require documentation such as pay stubs, tax returns, W-2 forms, and, in complex cases, expert testimony from forensic accountants or vocational economists. When a plaintiff is self-employed, has irregular income, or has no employment history, courts may rely on regional or national median household income figures as a baseline reference.

According to a 2021-2024 review of 5,861 settled personal injury cases by Brown & Crouppen, the average personal injury settlement was $55,056.08. However, this figure obscures enormous variation tied directly to the victim’s income level and the nature of the injuries. Catastrophic or permanent injuries with long projected work-life expectancies will generate damages multiples above the average.

| Key legal principle: The damages calculation for future lost earning capacity requires projecting what the plaintiff would have earned over their remaining work life, discounted to present value. Where the plaintiff’s pre-injury income is unclear, expert witnesses may use local or national median household income as the starting benchmark. |

2. Wrongful Death Claims: Median Income Impact on Settlement

Wrongful death claims under state tort law allow surviving family members to recover the economic value of the decedent’s support. Courts calculate this value by projecting what the deceased would have earned over their remaining work-life expectancy, applying adjustments for personal consumption, and discounting to present value.

The median household income impact on wrongful death lawsuit settlement values is substantial. A decedent earning above the national median will generate higher damages; one earning below will generate lower damages. This creates a documented disparity in the value of human life across income classes, a topic of ongoing legal and ethical debate.

In California, for instance, a wrongful death claim involving a tech professional earning $180,000 per year will calculate economic damages in the multi-million dollar range, while a claim involving a worker earning the state median of $100,100 will generate substantially lower awards even for identical injuries.

3. The Bankruptcy Means Test: Median Income as an Eligibility Gate

The Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 (BAPCPA) introduced the means test as a threshold filter for Chapter 7 bankruptcy eligibility. The means test is one of the most direct statutory uses of median household income in all of U.S. federal law.

Under the means test:

- A debtor whose current monthly income (CMI), annualized, falls below their state’s median household income for their family size is presumptively eligible for Chapter 7 liquidation bankruptcy.

- A debtor whose income exceeds the state median must complete a detailed expense analysis. If disposable income exceeds a statutory threshold, there is a presumption of abuse, and the court may dismiss the Chapter 7 petition or convert it to Chapter 13.

- Current monthly income is calculated as the average gross monthly income over the six full calendar months immediately preceding the filing date, the six-month lookback period.

The U.S. Department of Justice updates the applicable median income figures regularly using Census Bureau data. As of 2025-2026 filing periods, these figures vary significantly by state and family size. For California, the threshold for a single-person household differs substantially from that for a four-person household, with the latter exceeding $100,000 annually.

| Attorney tip: In bankruptcy practice, the distinction between a client who is marginally above or below the state median household income can mean the difference between a fast, inexpensive Chapter 7 case and a three-to-five-year Chapter 13 repayment plan. Accurate CMI calculation is therefore one of the most legally consequential tasks in consumer bankruptcy representation. |

4. Employment Discrimination: Wage Gap and Back Pay Calculations

Federal employment discrimination law under Title VII of the Civil Rights Act, the Equal Pay Act of 1963, the Age Discrimination in Employment Act (ADEA), and the Americans with Disabilities Act (ADA) all permit recovery of lost wages and, in some cases, front pay. The calculation of these damages relies heavily on income benchmarks, including median household income and median earnings by occupation, race, sex, and age.

The Census Bureau’s data showing that the female-to-male earnings ratio fell to 80.9% in 2024 is precisely the type of statistical evidence used in disparate impact claims. When a plaintiff alleges that a workplace policy disproportionately depresses earnings for a protected class, median income data for that class versus the comparator class forms the statistical backbone of the liability case.

Under Rev. Rul. 96-65, back pay received to satisfy a claim for disparate treatment employment discrimination under Title VII is not excludable from the plaintiff’s gross income for tax purposes. This means plaintiffs must account for the tax consequences of any employment discrimination settlement, a complexity their counsel must navigate at the time of settlement negotiation.

5. Family Law: Child Support and Spousal Maintenance

In family law proceedings, both child support guidelines and spousal maintenance (alimony) calculations require determination of each party’s income. When one party’s income is imputed (i.e., the court assigns an income figure to a party who is voluntarily unemployed or underemployed), courts in many states use the state or local median household income for a person of that education level and skill set.

Imputed income based on median household income prevents a party from artificially suppressing their support obligations by voluntarily reducing earnings. This use of median income as a floor is a protective mechanism widely embedded in state family law statutes and judicial guidelines.

6. Criminal Fines and Economic Penalties

While less widely discussed, median household income also plays a role in the calibration of criminal fines, particularly under sentencing guidelines that aim to impose proportional economic penalties. The principle of proportionality in punishment requires that a fine be painful but not crushing to a defendant of ordinary means, and ordinary means is often benchmarked to the median income of similarly situated individuals.

Federal courts applying the U.S. Sentencing Guidelines consider a defendant’s ability to pay fines, and median income data provides a reference point for what constitutes an excessive versus proportional financial penalty for a person of average economic means.

Legal Complications and Controversies Involving Median Household Income

The Mean vs. Median Debate in Damages Litigation

One of the sharpest legal disputes surrounding income-based damages is whether courts should use mean (average) or median income as the appropriate benchmark, particularly in wrongful death and lost earning capacity cases involving plaintiffs with no or minimal prior earnings history.

Plaintiffs’ attorneys typically prefer mean income as a baseline because it is higher and produces larger damages awards. Defense attorneys typically prefer median income because it is lower and reduces the damages exposure. The academic literature, including work published by the CESifo Institute for Economic Research, has examined this tension and noted that jurisdictions differ significantly in which metric they favor.

The legal argument for median income rests on statistical representativeness: median income better reflects what a typical person would have earned, uninfluenced by extreme outliers. The legal argument for mean income rests on the principle of making the plaintiff whole: if society as a whole generates a certain average level of wealth, a victim should not be assigned a below-average value simply because they had not yet reached their earning potential.

Geographic Income Disparities and Venue Selection

Because median household income varies enormously across states and counties, the choice of venue in personal injury, wrongful death, and employment litigation can materially affect damages outcomes. Attorneys engaged in multi-state litigation or cases with multiple viable venues are acutely aware that filing in a high-income jurisdiction can produce a higher damages award than filing in a low-income jurisdiction.

This creates a legitimate strategic consideration (proper venue selection) but also raises equity concerns: defendants in high-income states face substantially greater liability exposure for identical conduct than defendants in low-income states. Tort reform advocates have used this disparity to argue for uniform national damages standards.

Race, Gender, and the Valuation of Damages

The most ethically sensitive legal complication arising from median household income in damages litigation is the use of race- and gender-specific income data. If courts calculate lost earning capacity based on median income for a plaintiff’s specific demographic group, rather than a race- and gender-neutral national figure, plaintiffs from historically lower-earning groups receive smaller awards.

This practice has been challenged on equal protection grounds. Several courts have moved toward using gender-neutral and race-neutral income tables. The American Bar Association and various civil rights organizations have advocated for race-neutral economic projections on the grounds that historical wage disparities reflect systemic discrimination that the legal system should not perpetuate through its own damages calculations.

| Critical legal issue: The use of race- or gender-specific income data in damages calculations is an evolving area of law. Attorneys handling personal injury or wrongful death cases involving minority or female plaintiffs should be prepared to argue for race-neutral and gender-neutral actuarial tables, citing both equal protection doctrine and the public policy against perpetuating discriminatory wage patterns. |

Household Income in Class Action Settlements

Class action litigation involving large numbers of economically diverse plaintiffs presents challenges in allocating settlement funds. Courts and settlement administrators frequently use median household income as a factor in designing pro-rata allocation formulas, ensuring that lower-income class members, who may suffer disproportionate economic harm from the same conduct, receive proportionally greater relief.

Research published in ResearchGate examining the correlation between household income and settlement quality has found that settlement satisfaction is inversely correlated with income level in some categories of litigation, suggesting that current allocation methodologies may systematically underserve lower-income plaintiffs even when median income data is incorporated into the formula.

The Bankruptcy Means Test: Ongoing Litigation and Policy Debate

The use of median household income as the eligibility gate for Chapter 7 bankruptcy has generated substantial litigation since BAPCPA’s enactment. Courts have grappled with how to define the household, what income sources to include, how to treat irregular income, and whether regular financial contributions from non-debtor family members must be included in the current monthly income calculation.

In households with extended family contributions, particularly in immigrant communities where remittances flow both to and from the household, the median income threshold can produce inequitable outcomes. Courts have reached inconsistent conclusions on these issues, creating a patchwork of bankruptcy law across circuits.

Median Household Income Impact on Lawsuit Settlement Values

Understanding how income levels interact with settlement dynamics is essential for both plaintiffs and defense counsel. The following principles govern how median household income affects personal injury settlement outcomes:

Economic vs. Non-Economic Damages

Economic damages (medical expenses, lost wages, lost earning capacity) are directly income-sensitive. Non-economic damages (pain and suffering, emotional distress, loss of consortium) are less directly tied to income, though higher-income plaintiffs may succeed in arguing that their quality-of-life impairment is proportionally greater due to their active professional lives.

Multiplier Methods and Income

Many plaintiff attorneys and insurance adjusters use a multiplier method to calculate total damages, multiplying special (economic) damages by a factor of 1.5 to 5 depending on injury severity. Because special damages are tied to income, a higher median income jurisdiction will produce a higher baseline for this calculation, magnifying the total settlement figure.

Average Settlement Based on Income Level

While no single authoritative database tracks average settlement by income level, the following patterns are well-documented in legal literature and practitioner experience:

- Plaintiffs with income above the national median ($83,730) typically command significantly higher economic damages components.

- Plaintiffs below the median may still receive comparable non-economic damages, but the economic damages floor is lower.

- In states with high median incomes like California ($100,100), New Jersey (~$105,000), and Maryland (~$102,000), baseline settlement values for equivalent injuries are measurably higher than in lower-income states.

- Medical malpractice claims in 2024 averaged $435,000 per payment nationally, but high-income state claims can substantially exceed this figure when the plaintiff was a high earner.

Future Earning Capacity: The Biggest Driver

For younger plaintiffs with permanently disabling injuries, the future earning capacity component of damages can dwarf all other elements. A 30-year-old California professional with a work-life expectancy of 35 additional years, earning the state median of $100,100, would have a gross future earning projection of approximately $3.5 million before discounting to present value and adjusting for personal consumption. A plaintiff in a lower-income state at the national median would project to approximately $2.9 million on the same inputs.

State-by-State Legal Implications: High vs. Low Median Income Jurisdictions

The 2024 American Community Survey reported that real median household income increased in 29 states between 2023 and 2024. The following highlights the legal significance of income variation by state:

- High-income states (California, New Jersey, Maryland, Massachusetts, Washington): Higher damages awards in tort cases, stricter bankruptcy means test thresholds, larger child support imputation benchmarks.

- Low-income states (Mississippi, West Virginia, Arkansas): Lower economic damages baselines, lower means test thresholds making Chapter 7 more accessible, smaller imputed income figures in family law.

- States with high income inequality (New York had the highest Gini index per 2024 ACS): Greater variability in damages outcomes within the state, larger disparities between high- and low-income plaintiff awards, more contentious debates about race- and gender-neutral income tables.

Frequently Asked Questions (FAQ)

Q1: What is median household income, and why does it matter in a lawsuit?

Median household income is the income level at the midpoint of all U.S. households, with half earning more and half earning less. In a lawsuit, it matters because courts use income data to calculate economic damages, including lost wages and future earning capacity. Your actual income, benchmarked against median figures, helps determine the dollar value of your economic loss.

Q2: What is the median household income in the United States in 2024?

The U.S. Census Bureau reports the national median household income in 2024 as $83,730, based on the Current Population Survey Annual Social and Economic Supplement released in 2025. This represents no statistically significant change from the 2023 figure of $82,690.

Q3: What is the median income in California, and how does it affect legal cases?

The median household income in California in 2024 was $100,100, approximately 22.7% above the national median. This higher baseline means California personal injury and wrongful death plaintiffs typically present higher economic damages claims. It also means the Chapter 7 bankruptcy means test threshold is higher in California, making it harder to qualify for liquidation bankruptcy without additional expense analysis.

Q4: How do courts calculate damages using income data?

Courts calculate economic damages by reviewing documented past earnings (pay stubs, tax returns, W-2s), projecting future earnings over the plaintiff’s remaining work-life expectancy, and discounting those projections to present value using an accepted discount rate. Where actual earnings are unavailable or contested, median household income for the plaintiff’s occupation, education level, or geographic area serves as the reference baseline. Expert witnesses, including forensic economists, are commonly retained to perform and defend these calculations.

Q5: Can median household income affect my bankruptcy case?

Yes, directly and significantly. Federal bankruptcy law uses your state’s median household income as the primary threshold in the Chapter 7 means test. If your annualized current monthly income (averaged over the six months before filing) falls below your state’s median for your household size, you are presumptively eligible for Chapter 7. If your income exceeds the median, you must complete a detailed expense analysis, and if your disposable income is sufficient, the court may deny Chapter 7 eligibility or convert your case to Chapter 13.

Adam Fermin

Chief Editor of Attorneys Magazine. Adam oversees the selection and verification of legal, marketing, and technology content. He focuses on distilling complex industry updates into actionable intelligence, ensuring every editorial piece meets the highest standards of professional relevance.

Disclaimer: This article is published for informational and educational purposes only and does not constitute legal advice. Income figures cited are based on publicly available U.S. Census Bureau, Federal Reserve Economic Data (FRED), and related government sources current as of early 2026. Legal outcomes depend on the specific facts of each case and applicable state and federal law. Consult a licensed attorney in your jurisdiction for advice specific to your situation.